Alices Wonderland 312% IRR Litigation Finance. Is This a Little White Pill?

Alices Wonderland 312% IRR Litigation Finance. Is This a Little White Pill?

Litigation Finance is a wonderland of risks and returns. Be prepared to swallow a little white pill of non recourse returns. Drink this I say. ( in depth follow on article from last weeks post)

It is not illegal for an outside entity to help fund another party’s lawsuit, and the practice, known as “third-party litigation funding” has become increasingly common in the USA, UK, and Australia. Typically, the outside party negotiates for a defined share of any proceeds from the suit.

There is an extraordinary amount of litigation funding going on in our justice system, and has been for a long time. Indeed, the litigation system is designed expressly to permit such funding (and not to require its disclosure, for sound policy reasons), and it would grind to a halt without it. What commercial litigation financiers do is part of a large and pretty boring business around commercial litigation – businesses suing each other. Other players in that world include insurers (the largest litigation funders around), banks, creditors, investors and corporate affiliates. Litigation funders exist because there is significant demand from corporate clients for financial solutions to ever-rising litigation costs and capital. This asset class, which lacks correlation to broader capital markets and macroeconomic activity, is appealing to this demographic of investors as well as individuals.

For many individuals and companies, pursuing a claim through litigation or arbitration can be prohibitively expensive and risky. Also, insolvency practitioners and lawyers often represent creditors who have suffered losses and do not want to suffer more. Even for those with the ability to pay, the uncertainty regarding both the total cost and the timescale to conclusion can make pursuing a claim an unattractive prospect.

Litigation funding is the provision of financial support to a claimant in a legal case by an unconnected third party in return for a share of the award assuming the case is won. I will discuss in detail the risks and returns in this paper.

In many jurisdictions, the cost of capital for the borrower is not recoverable from the defendant. The investor typically likes to see a claim value at a 10x multiple to make the investment case. Investors are also interested in post judgment claims because the claim has a judgment value. It is therefore enforceable judgment in any jurisdiction. Essentially, a litigation funder provides non-recourse legal finance to claimants in order that they can finance their legal fees and expenses. Claimants have no out-of-pocket expenses at the outset of the case. No plaintiff acting in his own financial interest would walk away from the one defendant with the guaranteed wherewithal to pay up nor would a lawyer working on contingency advise such a strategy.

The model is different from the more familiar models special situation investors are accustomed to. Funds investing in claims found in the court house or in pre-bankruptcy are usually post judgment, or in transparent procedures.

Litigation funding works as a complete transfer of the financial risk associated with pursuing the case: if there is no recovery at the end of the case, the litigation funder’s investment is lost and the claimant has no debt to repay.

Investors are divided into three distinct groups.

- Funds specifically set up to invest in claims include: Burford Capital, Vannin, Therium, Bentham, Woodsford, Augusta, Orchard Capital have offices around the globe . They manage funds on behalf of institutional investors .

- Hedge Funds, credit and distressed funds: Traditional asset managers including Orchard Asset Management. They are one of a handful of structured credit funds creating a litigation funding product for institutional investors. Orchard hired ex Deutsche debt and equity banker and lawyer Adrian Chopin in 2015 to develop a litigation product suite. Orchard invests in smaller claims across Europe, or syndicate larger claims with other investors. So far returns have been a whopping 1000%. This is because they have not lost their investors money. However Chopin tells me that this will certainly change and they will eventually lose a claim. The estimated returns are a respectable 30% IRR. Given the risk involved this is a reasonable expectation. They are accepting new investor’s capital with the goal of raising a new fund in 2017. They are always interested in purchasing new claims, with a typical size of $500,000.

- Crowdfunding/Fintech. The third sector experiencing rapid growth is legal Fintech. Still in its infancy, but gaining momentum in the US and Europe.

What’s in it for investor? In return for shouldering all the financial risk, funders buy a percentage of the damages recovered or a multiple of the costs funded assuming the case wins. If the proceedings fail, the funder gets nothing and may face liability for the other sides’ costs, depending on the jurisdiction.

What do all three segments look for in a case? A good case consists of these elements: corporate and company matters, professional negligence Tax/VAT antitrust, financial services and banking, insolvency, intellectual property high value divorces, breach of contract claims and tort. In addition to the due diligence on the documents, selection criteria for plaintiffs are a key component to a successful outcome of a case. Legal merits are considered, claims value, estimated time to resolution. The defendant must have the financial strength to meet the claim or enforcement of the judgment. Claimant must have a credible legal team and strategy. Funding costs are proportionate to the claim value; Small claims with large costs do not work economically.

Investor Group 1: This is where the 3 groups differentiate: The top end of the market is well covered and serviced. With the exception of Woodford, typical equity investment is $1million with a claim size of $10m. Funders fund no more than 10% of the total claim amount. Expected Returns are 300%. Woodford will look at claims sub 10m with an equity investment of $400,000 and up. Expected returns are also 300%.

Investor Group 2. : Orchard and other funds are investing in trades originated by group 1. Orchard also invests in smaller trades on crowdfunding platforms. The fund pays a return to its investors, takes care of DD and managing the legal process. Takes the risk out of the investment. Returns are 12-15%. Fees to investors are taken from the funds management and performance fees contained in the mandate.

Investor Group 3: Using Technology to level the playing field for smaller claims:

Crowdfunding Legal Tech is where it gets interesting but also carries more risk. This is the only section of the market open to private and institutional investors. There are 3 players active in plaintiff’s commercial litigation space. Each uses a Fintech variant crowdfunding model.

www.Lexshares.com is a Kickstarter for plaintiffs who don’t have pockets deep enough to hire Quinn Emanuel , let alone pay for experts witness, investigators and everyone else in the lawsuit food chain. Plaintiffs use the website to crowdfund their lawsuits in exchange for giving funders or investors a cut of the judgement or settlement. Individuals can invest as little as $2,500. In July, LexShares opened the platform to institutional investors such as hedge funds. Jay Greenberg is the co-founder and CEO of LexShares, based in New York City, which launched in November 2014. LexShares’ model helps connect accredited investors with pre-vetted investment opportunities. A breakdown of the number of plaintiffs, accredited investors, institutional investors, law firms, lawyers, and whoever else is using it. The majority of these users are individual accredited investors looking to invest in legal claims. Deal flow has been strong with greater than $25 million of funding requests generated through our online platform. More than 85% of funding applications come from claimants themselves. These claimants are typically the CEO, CFO or general counsel applying for funding on behalf of their corporation. The remainder of requests come from attorneys representing these corporate plaintiffs. Interestingly, we also have some law firms registering on the platform as well to invest in cases. Typical case sizes for investment require $100,000 to $1, 00,000 of investment with a use of proceeds including legal fees, expert witness, and working capital. Cases may be at different stages of litigation. Lexshares and Alter enable investors with little to no legal background to invest in cases while also enabling those with legal training to take a more in-depth look at the cases. The cases are monitored post investment and investors are apprised of courtroom activity related to the investment on the platform.

This is a pro bono site run by a group of lawyers in Geneva, Switzerland. The team of lawyers review the case to ensure it is legitimate. Invest4Justice came in to existence due to the accessibility to few people who can access justice with quality legal counsel, even when they have highly meritorious cases, for purely financial reasons. As of now, Invest4Justice supports equal admittance to righteousness and in this endeavour; the experts help people in their crowdfunding campaign to bear the expenses while their cases are still in the process.

Invest4Justice, founded in 2013, is the leading litigation crowdfunding website in the world. It is entirely free to use and open to litigants globally. As this is a pro bono site, there are no fees paid by either party. Augusta is an investor and sponsor. It enables the crowdfunding of legal disputes by an unlimited number of individuals in return for success fees (also known as contingency fees), often offering returns of 500% or more to potential investors. The return is reflected in the risk, data quality, borrower quality is highly speculative. Invest4 Justice is a peer to peer lending model similar to Lexshares. Investors are looking for superior rates of returns. Investors can earn excellent returns of 300% or more. The site allows plaintiffs to post evidence, a video and run a funding campaign. The quality and type of cases vary greatly. So does the risk. campaigns run 90 days or less.

Current cases on this site include: Breach of Contract and Fraud case against Deutsche Bank is the only case where there is a counsel opinion letter available with an 80% chance of recovery. This case has the right elements; liquid defendants, and ability to pay enforceable a judgment, good jurisdiction, solid legal representation and a credible plaintiff, with evidence to support the claim. The return for investment of over $10,000 per investor is 312%. The remainder of the cases appear to have poor data quality, unknown chances of recovery, and unknown plaintiff and legal representation abilities. If interested as a private investor you should check out the claims on the site. Augusta Capital has seeded the site using it as an origination point.

Commercial litigation case for loss of earnings paying a 33,333. % return. Reflects the risk and chances of recovery are highly speculative.

IRS Whistleblower case 427% returns. $56M tax fraud the government will pay $5M. ticket size is $350,000 return of 6x on investment. Attorney who is a tax attorney who calls this case “one of the best whistleblower cases ever”.

Ticket sizes range from $15,000 to $500,000. Avg. Ticket funding size is $50.000. invest4 takes no fee and once the investment is agreed drafts the contracts between the investor borrower and counsel to protect the parties interests.

www.alterlitigation.com

In Europe and France. A wide spectrum of litigation both in France and Europe, and also international arbitration. Alter Litigation funds cases not only for individuals, companies, public bodies, charities but also group actions and class actions. The funds underwritten finance legal fees, disbursements and expert fees in return for a percentage of the recovered amount reflecting risk taken, claim size and level of costs. Alter also invests in insolvency procedures which sets it apart from the other crowdfunding and third party funding sites.

Alter does not have a minimum case size but looks to viability of the case. Alter does not charge a set percentage of amount recovered. The success fee is negotiated between the plaintiff and the fund based on the risk profile of the case. They do not charge a multiple of the amount advanced.

Crowdfunding fees: registration on the sites is free. Lexshares takes an application for professional investors who certify that they qualify under the US IRS scheme for qualified investors. typical fee is 20% of funds raised. Investors are not charged upfront management fees. Lexshares take a 20% carried interest in each case they fund, and receive a portion of the profits returned to investors from proceeds recovered. They also make money from a portion of funds raised by the plaintiffs, only if the fundraising goal is successful. To date, the founders have said tall cases they take have a 100% success rate. Recently launched case raised $175,000 in 74 minutes and was oversubscribed.

What are the risks?

Lexshares claim to not have investors lose money on a case funded through the platform. The other 2 sites do not disclose the risks. Lexshares have been active for 6 months. Cases still pending have not been adjudicated and are in process. Funds are exchanged when the cases are fully subscribed.

What is the typical investment horizon? Avg. time to execution is 90 days.Avg. investment horizon is 30 months to trial.

Legal ownership, security interest: If a claim meets criteria, plaintiff and counsel receive a term sheet and funding agreement. After the terms are accepted, a final review is performed. There is no transfer of ownership in the claim. The term sheet creates a lien on the case. The lien has priority for recovery prior to counsel and the plaintiff recovery. In most cases, if the recovery is less than the expected amount, the investor recovers the investment but not more than the plaintiff’s recovery.

What are the main concerns concerning crowdfunding?

“The Lawyer” voiced 6 main concerns concerning litigation crowdfunding: (1) there would be future regulation in this field, (2) it was more difficult to determine that a case would be won and recovery would be successful than determining whether a loan would be paid back as on a peer-to-peer lending exchange, (3) only high net-worth individuals should be able to invest in litigation due to its risks, suggesting a minimum amount of capital of GBP 2 million as with third-party funders that have voluntarily signed up to a code of conduct, (4) the risk of privileged information about a case being made public, (5) the question of adverse cost risk, where the Arkin case established the funder’s costs liability could not exceed their amount of contribution and (6) the need for additional funding as a case proceeds

Due diligence: The opportunities undergo rigorous due diligence process by legal staff. This is standard at the large funders, Lex Shares and Alter the first French litigation funding site. The majority of participants have their own in-house due diligence, however some funds use outside law firms for due diligence on larger claims. This increases costs, causes delays in funding. Access and data quality tends to be very good on cases that are well developed. The earlier stage cases have less data and documents. Cases already filed have documents available from the courts.

Access to data: Case documents are held on a secured server, or data room with the exception of invest4justice. Plaintiffs load the docs onto the site, and are password encrypted.

Legal team: Plaintiffs must be represented by experienced counsel with a strong track record of success in the related legal area.

Defendant’s creditworthiness: Defendants must be well-capitalized entities with an ability to pay any damages awarded as a result of litigation.

The cost of litigation: The expected costs of the claim must be foreseeable. An estimated budget is required from counsel to consider a case. The larger funds expect to see a litigation plan, or executive summary, written by the plaintiffs’ counsel. The plan is expensive and time consuming to write. The plaintiff’s lawyers need to have the skills to write the plan. This includes a summary of the information about the case, plaintiff, defendant, damages, judge, and jurisdiction. Investors are provided with publicly disclosed court documents about the case.

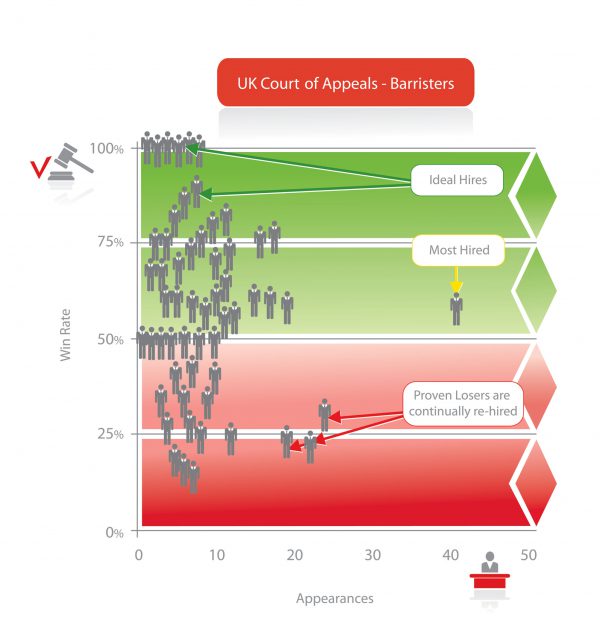

Using legal tech to derisk large claims: Founded in 2014 and headquartered in Miami, Premonition is an artificial intelligence system that is used to mine the information in “big data” to determine the effectiveness of individual attorneys. The company possesses the largest litigation database in the world, exceeding the size of every major legal database combined. The company recently closed a seed funding round at a valuation of $100 million. The analysis conducted by Premonition provides information relative to litigators winning percentages before specific judges. This eliminates what is seen as a very unfair advantage in litigation. The process produces better than a 30 percent improvement for companies who choose attorneys based on the analysis.

Unwin concludes by explaining, “Premonition provides an arbitrage between the market perception of a lawyer’s capabilities and success rates and reality. This shows that some lower-cost attorneys are much more effective in certain types of cases than the most expensive large firm partners.” Just how good is Artificial Intelligence attorney selection? “The choice of Counsel is worth an average 30.7% of the verdict,” claims Premonition CEO, Guy Kurlandski. “Over a large portfolio of litigation this can easily save an insurer hundreds of millions of dollars. What’s more your legal fees are often less.” Why is that? “We’ve found little correlation between hourly rate and outcome,” Kurlandski explains. While big firms (usually among the more expensive) tend to be 6.98% better than their competitors, simply picking top 20 performers per case type and Judge allows claims managers to take advantage of cheaper, overlooked talent. This technology is very cool, innovative and deadly to the opponent.

Regulatory:

http://associationoflitigationfunders.com – All organizations are voluntary. Code of Conduct, Key protections is afforded to clients, including clarity on issues of control of case strategy, approval of settlements and withdrawal from cases. The Code of Conduct for Litigation Funders was published by the Civil Justice Council – an agency of the UK’s Ministry of Justice – in November 2011, and the Association of Litigation Funders has been charged with administering self-regulation of the industry in line with the Code. It was written after months of research by a high-level Working Party that included senior lawyers, academics and business managers.

https://americanlegalfin.com is the American voluntary organization, members are personal injury funders and very few are commercial. There is currently no commercial litigation regulators all are voluntary. The US is still developing. The industry lacks transparency; there are many funders that charge high interest rates to unwitting plaintiffs who are vulnerable to becoming victims.

Key points of the voluntary regulatory schemes:

- Capital adequacy of funders

- Termination and approval of settlements

- Control

- Summary: In any investment, the most difficult aspect to the process is origination of good quality claims. The firms mentioned here run professional platforms with experienced in house and external legal and due diligence teams. The investment process mirrors the process special situations investors are familiar with. Investors are scanning the globe for yield. Is litigation funding the next source of trades? The asset has been around for about 25 years. Yet it still appears to be in its infancy. Much legal framework needs to be done to create more transparent opportunities for investors.

Published on September 19, 2016

{kind=link}

{kind=link}

{kind=link}